Hello, I'm

Jose Márquez Jaramillo

Quantitative Analyst & Developer

Building data and quantitative intensive applications for asset and wealth management.

Featured Work

Production-grade systems combining deep learning with quantitative finance

Reinforcement Learning for Cryptocurrency Portfolio Management

Deep RL framework comparing DQN, DDQN, and REINFORCE agents against classical optimization for crypto trading with rigorous evaluation methodology.

View Project

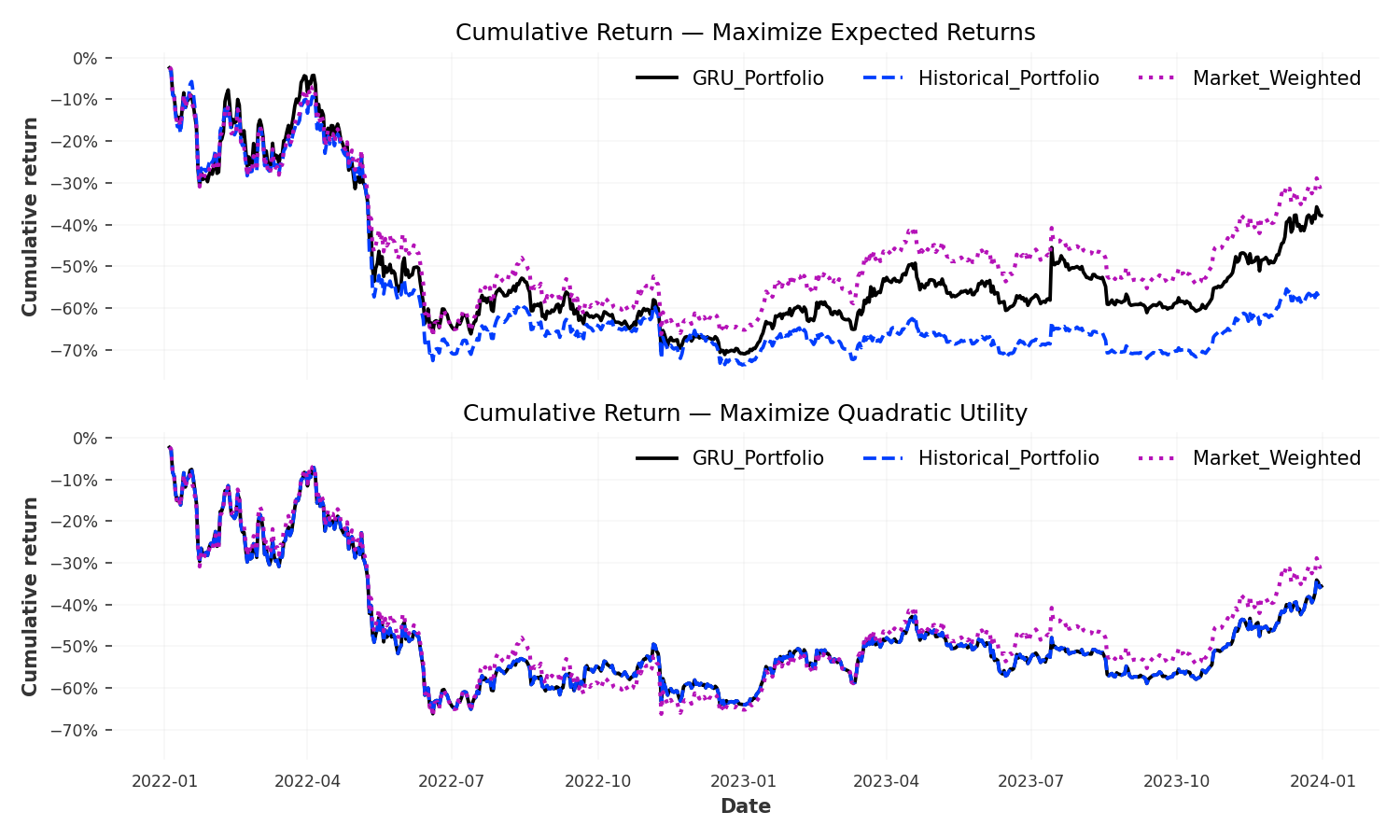

Kallos: GRU-Powered Cryptocurrency Trading System

End-to-end deep learning trading system combining neural network forecasting with portfolio optimization and rigorous statistical validation.

View ProjectAbout

I build data-intensive applications for quantitative finance, asset and wealth management.

Currently SVP at Citi Wealth Investment Lab, I develop back-end solutions for investment analytics that serve wealth management teams. I'm also pursuing an M.S. in Artificial Intelligence at Johns Hopkins University, focusing on machine learning and reinforcement learning applications in trading systems and portfolio management.

What drives my work is bridging the gap between quantitative research and production systems—building analytics platforms that wealth advisors can actually use to make better investment decisions.

Core Expertise

Specialized capabilities at the intersection of quantitative finance and machine learning

Production Analytics Systems

- Back-end solutions for wealth management platforms

- Enterprise investment analytics tools

- Tableau, Python, SQL integration

Algorithmic Trading Development

- Neural network forecasting systems

- Portfolio optimization & backtesting

- Walk-forward validation & statistical testing

Financial Data Infrastructure

- ETL pipelines with PostgreSQL storage

- Technical indicators & market data APIs

- Async processing & data quality validation

Applied Machine Learning

- Deep learning for financial forecasting

- GRU networks & custom loss functions

- Hyperparameter optimization & MLOps

Let's Build Something Together

Interested in collaborating on quantitative finance, machine learning research, or production ML systems?